With the U.S. presidential election weeks away, plenty of volatility catalysts could shift the market despite its solid performance year-to-date.

Cracks in the system have been appearing in recent months. We dive into three: a weakening labor market, Warren Buffett's cautious stance, and the potential presence of structural inflation.

Labor Revisions Flash Alert

After last month's labor revision that saw 800,000 fewer jobs added, the August U.S. payroll report came lower than expected at 142,000.

Still, revisions from previous months paint an even worse picture.

July's payroll figure was revised from 114,000 to 89,000, and June's number nearly halved from 206,000 to 118,000. This data suggests that the labor market is weaker than expected. It raises questions about whether the August report has been overstated, too.

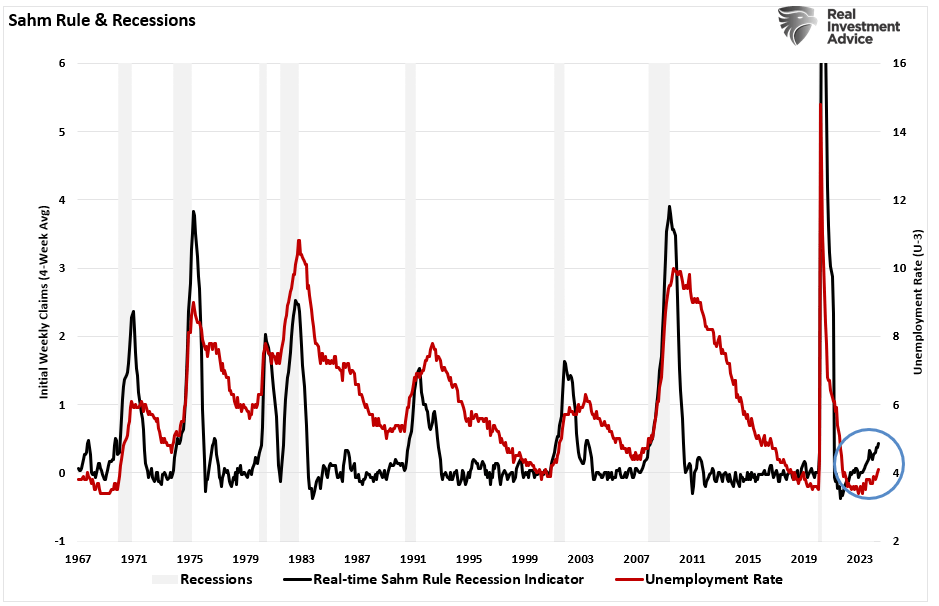

Furthermore, the Sahm rule, a recession confirmation tool, has been validated. After a 0.53 reading in July, the data ticked up to 0.57 in August, moving deeper into recession territory.

Sahm rule and recessions, Source: Real Investment Advice

Meanwhile, the yield curve has uninverted, with the two-year Treasury yield falling below the 10-year — a move that historically precedes recessions.

Buffett’s Cash Pile Sends A Message

Buffett has been slowly amassing almost $280 billion in cash, controlling over 3% of the T-bill market. In the second quarter, Berkshire Hathaway exited Paramount Global and Snowflake, reduced its position in Chevron, and nearly halved its huge position in Apple.

Furthermore, in Q3, Buffett started divesting from Bank of America, bringing the stake down to 11.1%. If this stake dips below 10%, the company could quietly exit the stake without disclosing the sale within the current regulatory framework of two business days.

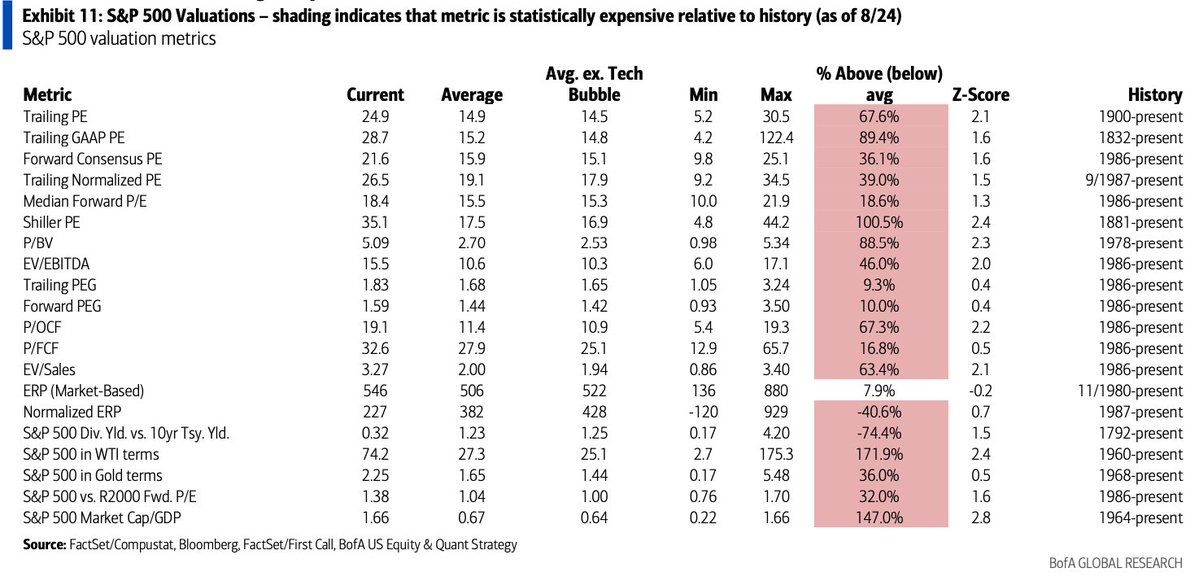

Buffett’s cash pile is now closing in on BofA’s market cap of around $300 billion. Meanwhile, per the bank’s global research unit — the S&P 500 is determined to be expensive on 19 out of 20 metrics.

S&P 500 valuation metrics, Source: BofA Global Research

Thus, it is unsurprising that Buffett struggles to find new investment opportunities.

Inflation As A Part Of The New Economy

While the latest CPI data print showed a 2.5%, the inflation rate has been slow to decline since FED's last rate hike in July 2023.

In fact, the July inflation rate was 2.89%, almost the same as 2.97% for July 2023. With modest seasonal oscillations, inflation has stabilized, and the market will need more than one data point to confirm a significant decline.

Stable inflation with a restrictive monetary policy means that this inflation could be structural — caused by persistent changes in supply and demand in the economy. In this case, lower supply caused by escalating deglobalization.

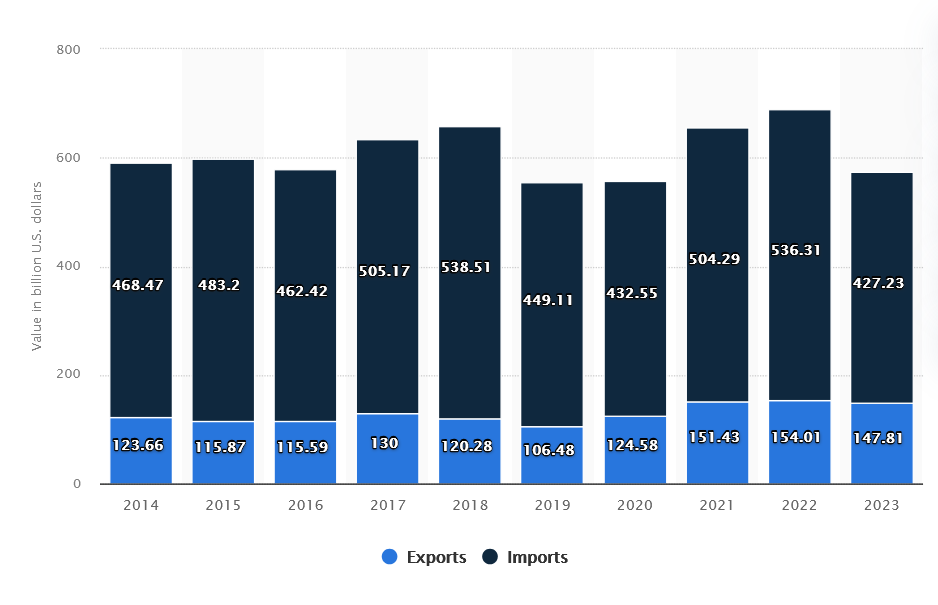

In 2023, US imports from China fell by 20% to $427 billion, and the trend might accelerate regardless of who sits in the White House in January. While Former President Trump initiated tariffs on Chinese goods, President Biden has increased tariffs on goods like steel, semiconductors, and EVs — bringing some up to 100%.

In the latest newsletter, EDC general partner Lyn Alden argued that the high debt-to-GDP ratio leaves the U.S. economy with two main choices. One is to keep interest very low despite periods of price inflation and debase all currency holders and bondholders.

The second one is to raise interest rates when needed meaningfully and contribute to a fiscal spiral of interest expense, hoping that the productivity growth from emerging technologies (such as AI) would be enough to offset the effect, contributing to the supply of goods and preventing the rapid rise in prices.

Now Read:

- Stocks Had Worst Start To September Nearly Ever – Here's Why

Image: Shutterstock